Advanced Quantitative Economics with Python

IRFs in Hall Models

21. IRFs in Hall Models¶

Contents

This is another member of a suite of lectures that use the quantecon DLE class to instantiate models within the [HS13] class of models described in detail in Recursive Models of Dynamic Linear Economies.

In addition to what’s in Anaconda, this lecture uses the quantecon library.

!pip install --upgrade quantecon

Requirement already up-to-date: quantecon in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (0.5.0)

Requirement already satisfied, skipping upgrade: sympy in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from quantecon) (1.6.2)

Requirement already satisfied, skipping upgrade: numba>=0.38 in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from quantecon) (0.51.2)

Requirement already satisfied, skipping upgrade: numpy in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from quantecon) (1.19.2)

Requirement already satisfied, skipping upgrade: scipy>=1.0.0 in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from quantecon) (1.5.2)

Requirement already satisfied, skipping upgrade: requests in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from quantecon) (2.24.0)

Requirement already satisfied, skipping upgrade: mpmath>=0.19 in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from sympy->quantecon) (1.1.0)

Requirement already satisfied, skipping upgrade: setuptools in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from numba>=0.38->quantecon) (50.3.1.post20201107)

Requirement already satisfied, skipping upgrade: llvmlite<0.35,>=0.34.0.dev0 in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from numba>=0.38->quantecon) (0.34.0)

Requirement already satisfied, skipping upgrade: certifi>=2017.4.17 in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from requests->quantecon) (2020.12.5)

Requirement already satisfied, skipping upgrade: urllib3!=1.25.0,!=1.25.1,<1.26,>=1.21.1 in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from requests->quantecon) (1.25.11)

Requirement already satisfied, skipping upgrade: idna<3,>=2.5 in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from requests->quantecon) (2.10)

Requirement already satisfied, skipping upgrade: chardet<4,>=3.0.2 in /usr/share/miniconda3/envs/quantecon/lib/python3.8/site-packages (from requests->quantecon) (3.0.4)

We’ll make these imports:

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

from quantecon import LQ

from quantecon import DLE

This lecture shows how the DLE class can be used to create impulse response functions for three related economies, starting from Hall (1978) [Hal78].

Knowledge of the basic economic environment is assumed.

See the lecture “Growth in Dynamic Linear Economies” for more details.

21.1. Example 1: Hall (1978)¶

First, we set parameters to make consumption (almost) follow a random walk.

We set

(In this example \(\delta_h\) and \(\theta_h\) are arbitrary as household capital does not enter the equation for consumption services.

We set them to values that will become useful in Example 3)

It is worth noting that this choice of parameter values ensures that \(\beta(\gamma_1 + \delta_k) = 1\).

For simulations of this economy, we choose an initial condition of:

γ_1 = 0.1

γ = np.array([[γ_1], [0]])

ϕ_c = np.array([[1], [0]])

ϕ_g = np.array([[0], [1]])

ϕ_1 = 1e-5

ϕ_i = np.array([[1], [-ϕ_1]])

δ_k = np.array([[.95]])

θ_k = np.array([[1]])

β = np.array([[1 / 1.05]])

l_λ = np.array([[0]])

π_h = np.array([[1]])

δ_h = np.array([[.9]])

θ_h = np.array([[1]])

a22 = np.array([[1, 0, 0],

[0, 0.8, 0],

[0, 0, 0.5]])

c2 = np.array([[0, 0],

[1, 0],

[0, 1]])

ud = np.array([[5, 1, 0],

[0, 0, 0]])

ub = np.array([[30, 0, 0]])

x0 = np.array([[5], [150], [1], [0], [0]])

info1 = (a22, c2, ub, ud)

tech1 = (ϕ_c, ϕ_g, ϕ_i, γ, δ_k, θ_k)

pref1 = (β, l_λ, π_h, δ_h, θ_h)

These parameter values are used to define an economy of the DLE class.

We can then simulate the economy for a chosen length of time, from our initial state vector \(x_0\).

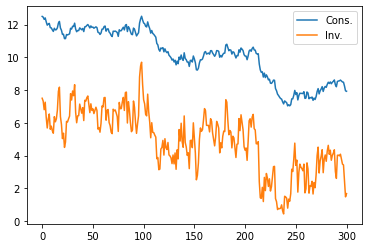

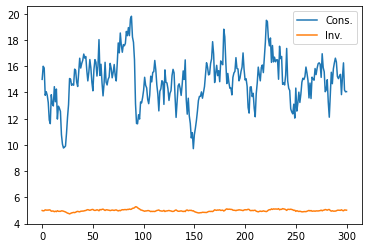

The economy stores the simulated values for each variable. Below we plot consumption and investment:

econ1 = DLE(info1, tech1, pref1)

econ1.compute_sequence(x0, ts_length=300)

# This is the right panel of Fig 5.7.1 from p.105 of HS2013

plt.plot(econ1.c[0], label='Cons.')

plt.plot(econ1.i[0], label='Inv.')

plt.legend()

plt.show()

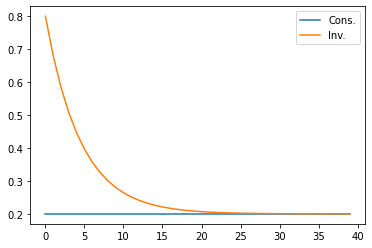

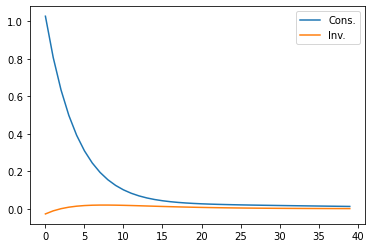

The DLE class can be used to create impulse response functions for each of the endogenous variables: \(\{c_t,s_t,h_t,i_t,k_t,g_t\}\).

If no selector vector for the shock is specified, the default choice is to give IRFs to the first shock in \(w_{t+1}\).

Below we plot the impulse response functions of investment and consumption to an endowment innovation (the first shock) in the Hall model:

econ1.irf(ts_length=40, shock=None)

# This is the left panel of Fig 5.7.1 from p.105 of HS2013

plt.plot(econ1.c_irf, label='Cons.')

plt.plot(econ1.i_irf, label='Inv.')

plt.legend()

plt.show()

It can be seen that the endowment shock has permanent effects on the level of both consumption and investment, consistent with the endogenous unit eigenvalue in this economy.

Investment is much more responsive to the endowment shock at shorter time horizons.

21.2. Example 2: Higher Adjustment Costs¶

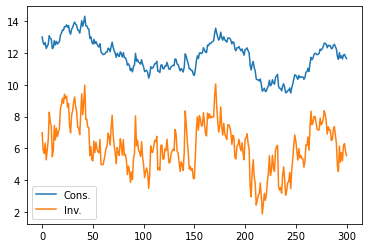

We generate our next economy by making only one change to the parameters of Example 1: we raise the parameter associated with the cost of adjusting capital,\(\phi_1\), from 0.00001 to 0.2.

This will lower the endogenous eigenvalue that is unity in Example 1 to a value slightly below 1.

ϕ_12 = 0.2

ϕ_i2 = np.array([[1], [-ϕ_12]])

tech2 = (ϕ_c, ϕ_g, ϕ_i2, γ, δ_k, θ_k)

econ2 = DLE(info1, tech2, pref1)

econ2.compute_sequence(x0, ts_length = 300)

# This is the right panel of Fig 5.8.1 from p.106 of HS2013

plt.plot(econ2.c[0], label='Cons.')

plt.plot(econ2.i[0], label='Inv.')

plt.legend()

plt.show()

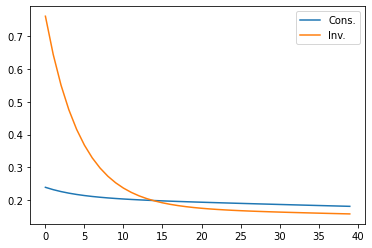

econ2.irf(ts_length=40,shock=None)

# This is the left panel of Fig 5.8.1 from p.106 of HS2013

plt.plot(econ2.c_irf,label='Cons.')

plt.plot(econ2.i_irf,label='Inv.')

plt.legend()

plt.show()

econ2.endo

array([0.9 , 0.99657126])

econ2.compute_steadystate()

print(econ2.css, econ2.iss, econ2.kss)

[[5.]] [[2.02678791e-12]] [[4.05357139e-11]]

The first graph shows that there seems to be a downward trend in both consumption and investment.

his is a consequence of the decrease in the largest endogenous eigenvalue from unity in the earlier economy, caused by the higher adjustment cost.

The present economy has a nonstochastic steady state value of 5 for consumption and 0 for both capital and investment.

Because the largest endogenous eigenvalue is still close to 1, the economy heads only slowly towards these mean values.

The impulse response functions now show that an endowment shock does not have a permanent effect on the levels of either consumption or investment.

21.3. Example 3: Durable Consumption Goods¶

We generate our third economy by raising \(\phi_1\) further, to 1.0. We also raise the production function parameter from 0.1 to 0.15 (which raises the non-stochastic steady state value of capital above zero).

We also change the specification of preferences to make the consumption good durable.

Specifically, we allow for a single durable household good obeying:

Services are related to the stock of durables at the beginning of the period:

And preferences are ordered by:

To implement this, we set \(\lambda=0.1\) and \(\pi = 0\) (we have already set \(\theta_h = 1\) and \(\delta_h = 0.9\)).

We start from an initial condition that makes consumption begin near around its non-stochastic steady state.

ϕ_13 = 1

ϕ_i3 = np.array([[1], [-ϕ_13]])

γ_12 = 0.15

γ_2 = np.array([[γ_12], [0]])

l_λ2 = np.array([[0.1]])

π_h2 = np.array([[0]])

x01 = np.array([[150], [100], [1], [0], [0]])

tech3 = (ϕ_c, ϕ_g, ϕ_i3, γ_2, δ_k, θ_k)

pref2 = (β, l_λ2, π_h2, δ_h, θ_h)

econ3 = DLE(info1, tech3, pref2)

econ3.compute_sequence(x01, ts_length=300)

# This is the right panel of Fig 5.11.1 from p.111 of HS2013

plt.plot(econ3.c[0], label='Cons.')

plt.plot(econ3.i[0], label='Inv.')

plt.legend()

plt.show()

In contrast to Hall’s original model of Example 1, it is now investment that is much smoother than consumption.

This illustrates how making consumption goods durable tends to undo the strong consumption smoothing result that Hall obtained.

econ3.irf(ts_length=40, shock=None)

# This is the left panel of Fig 5.11.1 from p.111 of HS2013

plt.plot(econ3.c_irf, label='Cons.')

plt.plot(econ3.i_irf, label='Inv.')

plt.legend()

plt.show()

The impulse response functions confirm that consumption is now much more responsive to an endowment shock (and investment less so) than in Example 1.

As in Example 2, the endowment shock has permanent effects on neither variable.